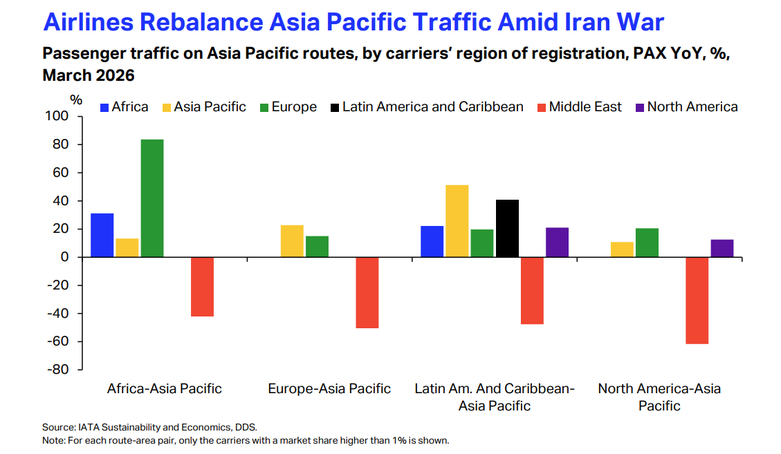

Air traffic flows across major intercontinental corridors have been significantly rebalanced following widespread disruption to Middle East carrier operations, highlighting the region’s structural importance as a global transfer hub. The Middle East traditionally plays a central role in connecting Asia Pacific with Europe, Africa, North America and Latin America, with Europe–Asia Pacific representing the largest share of connecting traffic routed through the region.

Recent operational interruptions, linked to geopolitical tensions and flight cancellations by Middle Eastern carriers, have triggered a noticeable redistribution of demand across alternative airline networks. European, Asia Pacific and African carriers have increasingly absorbed displaced traffic, particularly on Africa–Asia Pacific routes, where European airlines recorded year-on-year growth of more than 80% from a low base. On Europe–Asia Pacific corridors, both Asia Pacific and European airlines expanded traffic by around 15–23% year-on-year, reflecting a rapid reallocation of capacity.

Despite the shift in connectivity patterns, overall passenger demand to and from Asia Pacific remained resilient, increasing by 3.6% year-on-year in March 2026. However, capacity constraints outside the Middle East have led to record-high load factors, indicating that alternative networks have not fully replaced lost transfer capacity. The data suggests that the current market disruption is primarily supply-driven rather than demand-related, with airlines outside the region increasing capacity but still falling short of fully compensating for the reduction in Middle East hub connectivity.