The EU’s primary legislation governing Sustainable Aviation Fuels (SAF) is the ReFuelEU Aviation Regulation. By 2030, all aviation fuel supplied to aircraft operators at EU airports must contain a minimum 6% SAF blend, rising progressively in the years ahead. For airlines and cargo operators, the challenge is whether enough affordable SAF will be available.

Spanish startup, MacroCarbon, believes that pathway may come from an unlikely source: marine biomass. Founded by Prof. Dr. Mar Fernández-Méndez and Jason Cole, the company is currently carrying out a proof of concept with Airbus, Iberia, Repsol and Vueling, and claims it can produce SAF at around EUR 1,000 per ton at commercial scale. CargoForwarder Global spoke exclusively with Fernández-Méndez, MacroCarbon’s Chief Executive and Science Officer.

Not all SAF is created equal

SAF is often discussed as if it were a single product. In reality, different production pathways have very different economics, feedstock requirements, and scalability challenges. Used Cooking Oil (UCO) was initially considered the easiest route to scaling SAF. However, its limited availability has led to widespread concerns about fraud, such as the case uncovered in Malaysia in 2025, by a joint investigation by The Straits Times and Climate Home News, where cheap, subsidized virgin oils were allegedly mislabeled as UCO. SAF commands a substantial green premium, and bad actors have exploited the supply chain to bypass environmental regulations and drive deforestation.

eSAF and iSAF offer significant emissions reductions, but their economics remain challenging. Producing renewable hydrogen and capturing carbon dioxide requires large amounts of electricity, making these pathways substantially more expensive than conventional jet fuel.

According to Fernández-Méndez, UCO-based SAF currently trades at roughly EUR 2,000–2,500 per ton, while eSAF can reach EUR 7,000–9,000 per ton. MacroCarbon’s target is approximately EUR 1,000 per ton once fully deployed.

A third pathway uses biomass. Most projects focus on agricultural residues or forestry waste. The startup’s approach is different: marine biomass cultivated offshore. Fernández-Méndez believes the real advantage is not only environmental. The company argues that the ocean offers a scalable source of biomass while generating additional high-value products that improve the economics of SAF production.

According to IATA, scaling SAF production remains a major challenge for the aviation industry, with production volumes still far below what will be required to meet net-zero targets. While MacroCarbon’s target cost would be highly competitive if achieved, many emerging SAF pathways have historically encountered cost overruns during scale-up and commercialization.

Building a SAF supply chain offshore

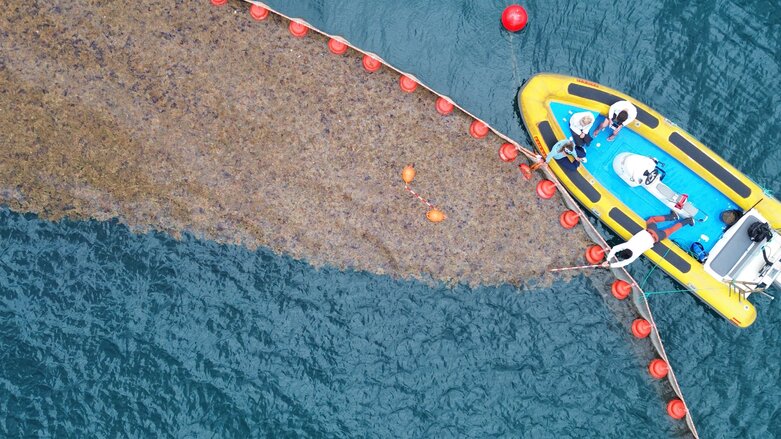

The Canary Islands-based developer is currently carrying out a proof of concept with Repsol, Airbus, Iberia, and Vueling. As part of the proof of concept, Vueling will test SAF blends produced by MacroCarbon in a laboratory-scale aircraft engine in Barcelona.

Under the planned deployment, the project consists of approximately 6 km² of aquaculture farms. This does not mean a single 6 km² installation, but multiple modules of 40,000 m² each, distributed across different locations and together totaling 6 km².

“Our current farm is located in the Port of Las Palmas de Gran Canaria, Spain. The 40,000 m² farm will be situated near the Oceanic Platform of the Canary Islands, which is located a few miles south of the Port of Gran Canaria,” Fernández-Méndez explains.

Can the economics work?

The biomass harvested from these farms would be processed in a dedicated facility equipped with six gasification lines using pyrolysis technology and a small-scale Fischer-Tropsch unit to convert the biomass into SAF.

While MacroCarbon’s feedstock is unconventional, its gasification and Fischer-Tropsch process relies on established technologies. The key challenge will be demonstrating that marine biomass can be produced at sufficient scale and cost.

According to MacroCarbon, the processing plant would require approximately EUR 90 million in investment, while the aquaculture farms themselves would require around EUR 10 million, bringing total project CAPEX to roughly EUR 100 million. The company estimates production costs could reach approximately EUR 1,000 per ton under its projected operating model. The figure remains subject to validation through commercial-scale operation. If achieved, that would place the fuel below current UCO SAF pricing and dramatically below most eSAF pathways.

The project is expected to produce around 8,000 tons of SAF annually. At approximately EUR 100 million in total capital expenditure and an annual SAF output of 8,000 tons, long-term profitability will depend not only on fuel sales but also on revenues generated from biostimulants, fertilizers, and other co-products.

Europe’s industrial challenge

The implications extend beyond passenger aviation. Air cargo operators face the same ReFuelEU blending requirements and SAF-related cost pressures as passenger airlines. Because fuel typically represents one of the largest operating expenses for freighter carriers, the availability of lower-cost SAF could directly influence future airfreight economics. If marine biomass-based SAF can be produced at the costs MacroCarbon is targeting, it could help reduce the green premium that cargo operators may ultimately pass on to shippers through SAF surcharges.

Fernández-Méndez is blunt about what she sees as Europe’s biggest challenges: fragmented and lengthy bureaucracy, combined with a venture capital system that remains heavily focused on software and AI.

The permitting process alone illustrates the problem. It took nine months to obtain approval for MacroCarbon’s farm in Las Palmas, despite the project being located in an area specifically designed for marine innovation and testing.

Financing is another challenge. While software and AI startups promise investors rapid returns, industrial projects require larger investments and longer timelines. “We need patient and non-dilutive capital and governments to get involved, basically China’s approach,” Fernández-Méndez says.

Europe has already paid a price for delaying difficult industrial decisions. The automotive sector is a recent example. Choices that once appeared too expensive became far more expensive once global competition accelerated.

Aviation has always been defined by flexibility and speed. The question is whether regulators, investors, and the industry itself can move fast enough to secure the SAF volumes it will soon be required to use. The challenge is even greater when alternative fuels must compete against an incumbent energy system that continues to benefit from decades of infrastructure, scale, and public support.

The real constraint may not be feedstock availability, but Europe’s ability to finance and permit industrial-scale SAF projects before competitors do.

How major SAF pathways compare

While UCO remains the dominant commercial SAF feedstock today, concerns over feedstock availability are driving interest in alternative pathways. Marine biomass is among the newest approaches and could offer competitive economics if commercial-scale production targets are achieved.

| SAF Pathway | Primary Feedstock | Typical Cost Range* | Scalability | Key Challenge |

| UCO-based SAF (HEFA) | Used Cooking Oil, waste fats | €2,000–2,500/ton | Limited | Feedstock availability and traceability |

| eSAF / Power-to-Liquid | Renewable hydrogen + captured CO₂ | €7,000–9,000/ton | High potential | Very high energy and electricity requirements |

| Agricultural Biomass SAF | Crop residues, forestry waste, agricultural by-products | €1,500–3,500/ton | Moderate | Feedstock collection and logistics |

| Marine Biomass SAF | Seaweed and other cultivated marine biomass | ~€1,000/ton (MacroCarbon target) | Potentially high | Commercial-scale validation still pending |